Income Tax Planning is one of Whitford's core services. Our ‘Tax Planning In Action’ series can show you ways to reduce the amount of money you pay in taxes over your lifetime.

Let’s break down how this is possible:

1. Robert was laid off at age 56 and after a full analysis of his retirement income needs, current assets, and financial goals, we determined he did not need to return to full-time work and could retire early.

2. Without much taxable income due to the loss of wages and a non-retirement account he could withdrawal from for living expenses, we examined that Robert would be in the 12% federal income tax bracket for the next several years.

3. However, we also projected that once his non-retirement account was depleted and he would need to start withdrawals from his IRA for living expenses, he would soon find himself in the 24% bracket or higher for the rest of his life.

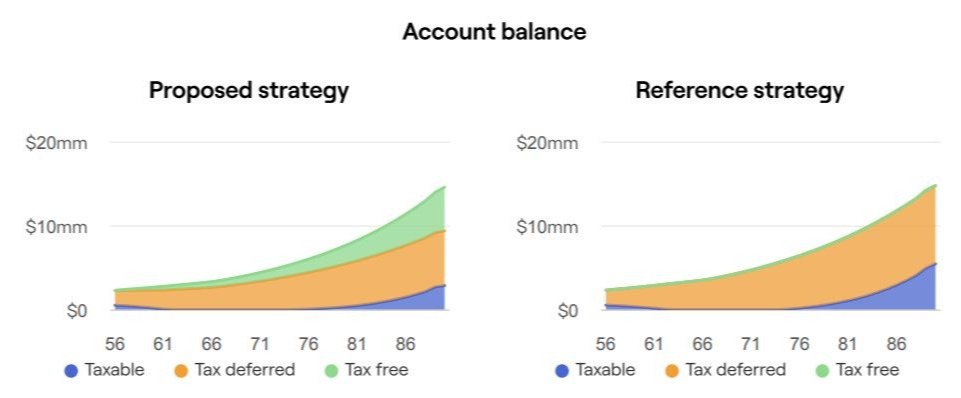

The Whitford Plan: Convert about $60,000 per year for the next 6 years from Robert’s IRA to a Roth IRA to “fill-up” or maximize the 12% tax bracket.

The Results:

- 38% of his assets by age 90 (projected) in a tax-free Roth IRA (vs. 0% with no planning), creating a much larger after-tax inheritance for his kids.

- An estimated $650,000 less in total taxes (projected) paid by Robert, simply by “filling-up” the 12% bracket, which allowed the Roth IRA balance to then grow and compound for many years tax-free and reduced his required minimum distributions (RMDs) from his IRA.

Note: Investment returns are hypothetical and do not reflect any specific investment or investment advice.

Summary: Every situation is unique including factors such as when to take Social Security, health insurance options with early retirement, paying the taxes on Roth IRA conversions, and many others. However, if your financial advisor is not reviewing your tax return and projecting your future tax rates, opportunities like Robert’s will likely be missed!

![]() Thanks for visiting! Schedule an Introductory Call to discuss what you want to accomplish and to see if we are a good fit.

Thanks for visiting! Schedule an Introductory Call to discuss what you want to accomplish and to see if we are a good fit.