You just did a Roth IRA conversion which seemed like a smart move for long-term tax planning. However, two years from now that conversion pushes your MAGI just over the next IRMAA tier, triggering thousands of dollars in additional Medicare premiums you didn’t see coming. This additional amount is doubled for a married couple.

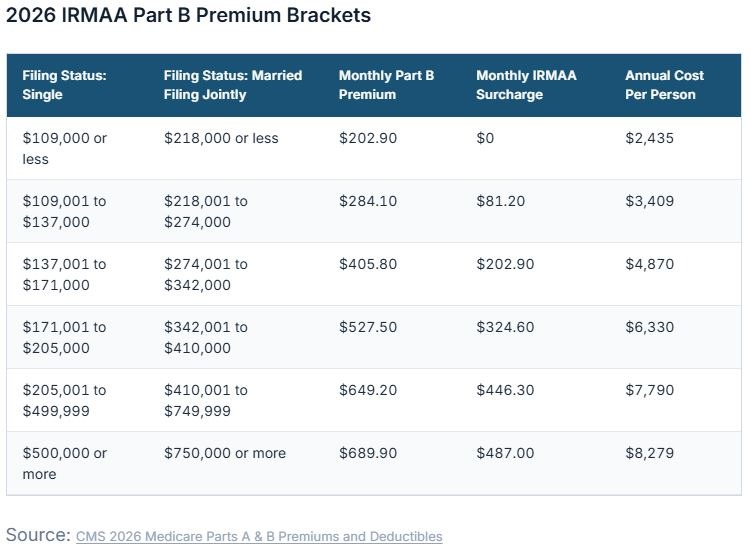

The Medicare premium surcharge is known as IRMAA (Income-Related Monthly Adjustment Amount). It is an additional amount added to your monthly Medicare Part B (medical insurance) and Part D (prescription drug coverage) premiums if your Modified Adjusted Gross Income (MAGI) exceeds established thresholds. The 2026 IRMAA brackets impose Medicare surcharges when MAGI exceeds $109,000 (single) or $218,000 (joint). IRMAA uses a two-year lookback, so income decisions today affect premiums paid in 2028.

For 2026, the standard Part B Medicare premium is $2,435 per year (or $202.90 per month). IRMAA surcharges are layered on top of this (and on top of your Part D plan premium) based on your MAGI from two years prior.

Key Planning Opportunities

1. Know Your Tax Bracket and Your "IRMAA Room"

If you are Medicare-eligible, it's important to know your “IRMAA room”, which is the dollars of additional income you can receive before crossing into the next IRMAA tier. If your income is well below the limits or far from the next tier you may be in good shape. Just remember that going even $1 over the MAGI limit will trigger the surcharges. This is where retirement income planning (i.e. which accounts you draw from and when) and IRMAA planning intersect. You can’t optimize one without considering the other.

2. Roth IRA Conversions - Within IRMAA Tiers

Roth conversions are one of the most powerful long-term tax planning tools, but they increase MAGI in the conversion year.

More on this topic - When Does a Roth IRA Conversion Make Sense?

A Roth conversion executed in 2026 affects IRMAA premiums in 2028. If you are currently below the IRMAA threshold and you’re planning a multi-year Roth IRA conversion strategy, you need to project your MAGI for every year in the sequence and check the IRMAA impact two years down the road. This gets complex fast! Each year’s conversion amount affects a different premium year.

The idea is to pay taxes when the rate is low, and then enjoy tax-free growth on any appreciation once inside the Roth IRA. Would you pay 12% now to avoid 24% later?

Example: A $50,000 Roth IRA conversion while still in the 22% bracket (up to $211,400 of MAGI for joint filers) is below the first IRMAA tier of $218,000, so no surcharge would apply. However, once your income crosses over $218,000 or higher for joint filers (see chart above), the first IRMAA tier would be reached. As you can see, it is critical when analyzing conversions to accurately project your income each year so you don't run into a negative surprise, like higher Medicare premiums a few years later!

Next Steps

Want to see how IRMAA planning works live with YOUR OWN REAL DATA? Or want to talk more about your retirement income goals? Schedule an Introductory Call to discuss what you want to accomplish and to see if we are a good fit.