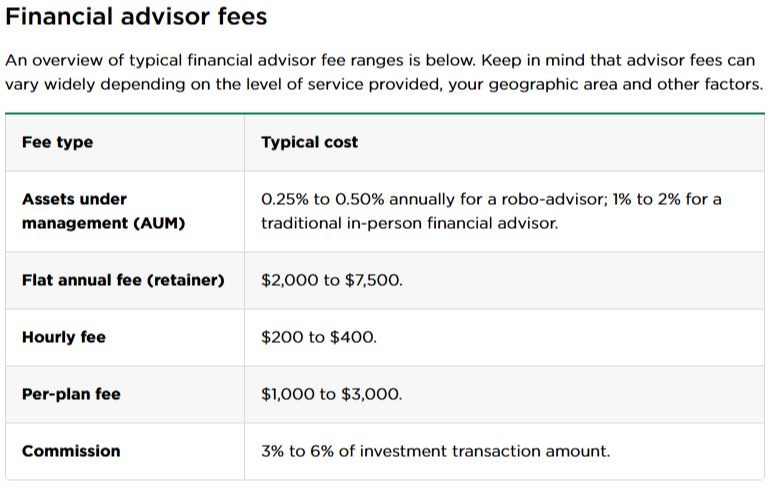

According to NerdWallet, most financial advisors charge based on how much money they manage for you (called Assets Under Management, or AUM), and that fee can range from 0.25% to 2% per year. However, there are several different ways to work with an advisor, and you need to understand what services you will receive for the cost.

The landscape for delivering and receiving financial advice is ever-changing, however, investors typically fall into one of three categories: Do-It-Yourself (DIY), Limited Advice, and Full-Service Advice.

Do-It-Yourself

The internet and social media have opened the doors to making almost any task a potential do-it-yourself one. If you enjoy learning new information, researching a topic for yourself, or want more control over your decisions, you are probably a ‘DIYer.’ However, just like researching a medical term or diagnosis, trying to learn everything there is to know about a financial topic in five minutes may not be enough time. Fortunately, there are lots of online tools available today.

Limited Advice

Let’s say you want someone to manage your portfolio and want to be able to ask questions as they arise. In this case a robo-advisor may be helpful. Typically, these services charge a lower fee (maybe 0.25% or more) to manage an investment portfolio based on your goals and use computer algorithms to maintain the strategy. Many of these financial institutions also offer the assistance of a company representative to provide limited additional guidance. Advisors that charge by the hour, on a project-based fee, or for an annual retainer with scheduled check-ins are also in this category. You may want help to do something straightforward without paying an ongoing fee for advice, such as set up college savings accounts or rollover an old 401(k) account.

Full-Service Advice

If you want to delegate the responsibility of managing your investments and overall finances, there are many full-service advisors. These advisory firms may bundle financial planning advice and money management as a combined service, so understanding their services and costs is important. Fees for ongoing advice usually average about 1% of the assets under management (AUM). In this service level you may receive tax and estate planning advice in addition to money management. In the AUM structure, you pay a percentage based on the amount of assets managed for you. If the fee is 1% of assets under management, and $500,000 of your money is managed, then you would pay a fee of $5,000 a year.

https://www.nerdwallet.com/article/investing/how-much-does-a-financial-advisor-cost

If you choose to pay for advice, understanding how advisors are compensated is critical. Many advisers try to eliminate conflicts of interest and act as fiduciaries by putting their client’s needs ahead of their own. According to The Free Dictionary, the word fiduciary is from the Latin word fiducia, meaning "trust," and is a person who has the power and obligation to act for another under circumstances that require total trust, good faith, and honesty. The good news is that the industry has been evolving towards a future with continued emphasis on putting the client first.

According to The National Association of Personal Financial Advisors (NAPFA), there are three primary advisor compensation models:

Fee-Only Compensation

This model minimizes conflicts of interest. It is the required form of compensation for members of NAPFA. A Fee-Only financial advisor charges the client directly for his or her advice and/or ongoing management. No other financial reward is provided by any institution, which means that the advisor does not receive commissions on the actions they take on the clients’ behalf. Compensation is based on an hourly rate, a percentage of assets managed, a flat fee, or a retainer.

Fee-Based Compensation (fee and commission)

This form is often confused with Fee-Only, but it’s not the same. Fee-based advisors charge clients a fee for the advice delivered, and they also sometimes receive payments for products they sell or recommend. In some cases, commissions are credited towards the fee, giving the appearance of a lower-priced option, but any outside compensation lessens the advisor’s ability to keep the client’s best interests first and foremost.

Commissions

Stockbrokers were initially needed to gain access to the market to buy and sell securities and charged a fee, called a commission, for each trade. NAPFA has always maintained that an advisor who is compensated through commissions is primarily a salesperson. A client working with a commissioned salesperson must always ask: Is this advice truly in my best interest, or is it the most profitable product for the advisor?

As you can see, it is essential to understand how your advisor is compensated for the advice you receive and whether they face hidden conflicts of interest. Make sure you understand and ask questions of any advisor about how their fees are structured and what services you will receive.

![]() Thanks for visiting! Schedule an Introductory Call to discuss what you want to accomplish and to see if we are a good fit.

Thanks for visiting! Schedule an Introductory Call to discuss what you want to accomplish and to see if we are a good fit.