*This post highlights Chapter 4 from Mike’s book, Achieving Financial Fulfillment.

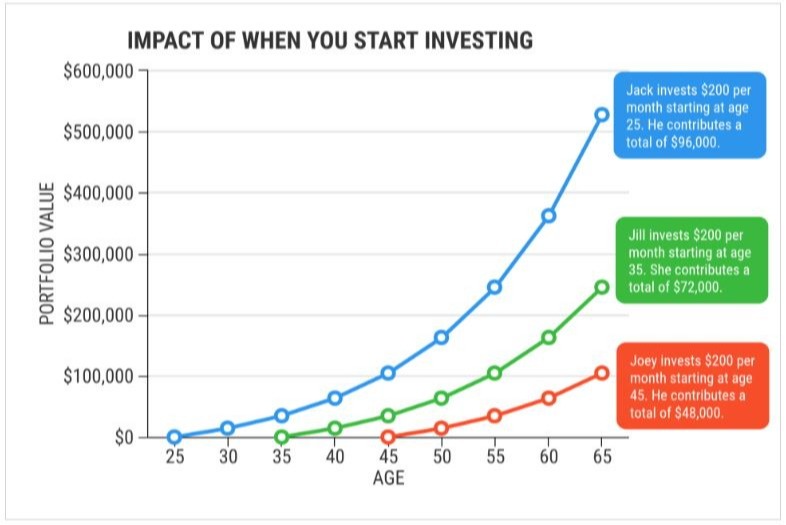

This famous quote by Benjamin Franklin can apply to many choices—especially those about personal finances. If we don’t take his message to heart, then a lack of planning can be costly. For example, look at the illustration below to see just how important it is to start saving and investing early. Starting just 10 years earlier at age 25 instead of 35, the projected investment balance for Jack at age 65 is more than double that of Jill! Joey is even farther behind by waiting until age 45 to start saving for retirement.

Hicks, Coryanne and Hellman, Nate. (3 Aug 2023). “Impact of When You Start Investing”. US News Money. https://money.usnews.com/investing/investing-101/articles/2018-07-23/9-charts-showing-why-you-should-invest-today. Assumes 7% growth per year.

An extremely important principle at work in the chart is compound interest. It’s possible for your money to make more money for you with no additional effort!

Let’s look at how saving early can make a difference: If you invest $10,000 and earn 5% interest in the first year, you would have made $500 ($10,000 * 0.05) in interest and have a total of $10,500. In the next year, you start with $10,500 invested at the same 5% interest, and it now earns you $525 ($10,500 x 0.05) in interest. So, your $500 earned in the first year made you an additional $25 ($500 x 0.05) of interest in the second year without any additional contribution from you, and so on and so on over time. This is how little numbers can become much bigger!

Also, setting up an automatic savings or investment plan is critical. No matter how small you start, you won’t miss it if it’s out of sight, out of mind. For example, you could have a certain dollar amount from each paycheck go into a savings account. Further, you could put a fixed percentage of your salary into a retirement account, such as a 401(k), in order to make sure you save on a regular basis and learn to live on what is left over.

As you can see, financial planning is a process to help you achieve your goals over time, not just a once- and-done event. It is also about much more than managing investments to get the highest return. Investments are a key component, but there are many other items that should be considered.

Set Realistic Goals

The first step is to set realistic goals for where you want to be in the future. If you prefer, you can work with an advisor who can help you to get organized. A written statement of your goals or a detailed plan can be developed to create a point of reference. Saving for retirement may be your most important long-term goal: you’ll likely have other financial goals, too. Maybe you would like to save for a vacation, pay down your debts, or buy a house in the near future.

Assess Your Investment Options

The second step is to assess your investment options. Investing that involves the use of stocks should only be considered when the time frame is long-term, generally five years or more. This is due to volatility and short-term declines that should be anticipated because of the many factors that could impact the value of a business. These can include changes in the company leadership, competition in the industry, or outside influences, such as geopolitical events or changes in the overall economy.

Determine Your Asset Allocation

The third and final step once your time horizon is understood, is to determine the asset allocation (or mix of stocks, bonds, etc.) to be used to achieve the goal. This is determined by taking into account the desired financial outcome and your risk tolerance (how much risk/reward potential is acceptable). Other factors to consider include how much money to set aside, your current sources of income, other investment and/or retirement accounts available, and the potential income tax implications of investing.

There are many choices when it comes to investment strategies. A simple way to group them is to identify them as aggressive, moderate, or conservative. Determining the rate of return that will be needed or what you assumed in your projections is an important part of planning how you will reach your goals. From this information, an initial asset allocation can be determined. The asset allocation should be revisited over time to determine whether your investment strategy should change and to monitor progress towards your goals.

The asset allocation between stocks, bonds and cash is said to be the single greatest factor in influencing portfolio returns. That means that the specific stock, mutual fund or ETF you buy is less important than you may think. Obviously, finding the next great company and buying it when the price is low would be nice as well, but that is much less likely and you should focus on what you can control. That is 1) what level of risk you are willing to assume and 2) diversifying in a way that allows you to capture the returns of the market over time and 3) reacting appropriately to what happens next in the market (or in many cases not reacting at all!).

Investing with a target asset allocation in place works because it does not rely on you needing to jump in and out of the best performing categories. It allows you to stay focused on your long-term goals. The inevitable volatility in the market then creates opportunities to rebalance your portfolio back to the target allocation.