Income Tax Planning is one of Whitford's core services. Our ‘Tax Planning In Action’ series can show you ways to reduce the amount of money you pay in taxes over your lifetime.

In Part 1, a client was considering a $50,000 sale of investments that would result in a $40,000 long-term capital gain. The original investment of $10,000 (or cost basis) had grown to $50,000, leaving her with a $40,000 gain. The tax rate on this was 15%, but why?

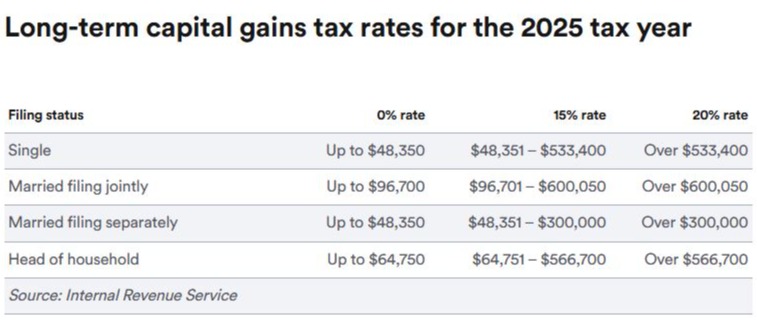

Her tax status is Married Filing Jointly and her taxable income was $200,800, including the capital gain. You can find all the rates in the table below, hers is 15%, found in the second row and the middle column.

Short-term capital gains vs. long-term

Short-term capital gains tax is applied to profits from selling an asset you’ve held for less than a year. Short-term capital gains taxes are paid at the same rate as you’d pay on your ordinary income, such as wages from a job.

Long-term capital gains tax is applied to assets held for more than a year. These rates are typically much lower than the ordinary income tax rates, which range from 10% to 37% in 2025.

At Whitford Financial Planning, we have found many opportunities clients didn't even know they had in the left-hand column of the chart, the 0% rate. For these income levels, there is no tax on capital gains! For example, if you file Married Filing Jointly and your taxable income is $76,700, you have room for a $20,000 long-term capital gain at $0 additional federal tax! ($76,700 + $20,000 = $96,700 combined). Income tax planning is all about paying taxes when the rate is the lowest and looking for these opportunities each year. They may come when you stop working, change jobs, or your taxable income changes for other reasons.

Strategies for making the most of investment losses

Stock market down this year? One strategy to offset your capital gains liability is to sell any underperforming securities, thereby incurring a capital loss. Realized capital losses could reduce your taxable income by up to $3,000 a year. Additionally, when capital losses exceed that threshold, you can carry the excess amount into the next tax season and beyond. For example, if your capital losses in a given year are $10,000 and you had no capital gains, you can deduct $3,000 from your regular income. The additional $7,000 loss could then offset capital gains or taxable earnings in future years. This strategy allows you to rid your portfolio of any losing trades while capturing tax benefits. Note: You must wait at least 30 days before purchasing similar assets after you sell, otherwise, the transaction becomes a “wash sale” and the IRS will not allow you to take the loss.

![]() Thanks for visiting! Schedule an Introductory Call to discuss what you want to accomplish and to see if we are a good fit.

Thanks for visiting! Schedule an Introductory Call to discuss what you want to accomplish and to see if we are a good fit.

Note: Depending on your state of residence, you may still owe state income tax on capital gains. Figures were rounded for simplicity. Also, the investment returns are hypothetical and do not reflect any specific investment or investment advice.