If your parents worked hard, saved and invested over the years, you may find yourself inheriting an IRA someday. But are you really prepared to receive it and understand the tax implications? The SECURE Act of 2019 removed the ability for most non-spouse/non-charity beneficiaries to stretch the required inherited IRA distributions over a lifetime, and instead changed it to require all of the money to be withdrawn by the end of the 10th year after death (for deaths in 2020 or later). Not everyone started annual RMDs back in 2020 because the law was unclear and has since been updated. As of mid-2024, annual RMDs were not required for years 1-9, but will be required starting in 2025. Then, the remaining IRA account balance has to be withdrawn by the end of the 10th year. So whether you are inheriting $100,000 or $1 million, you have to fit that amount of income from your IRA withdrawals into the next 10 years!

See the need for some serious tax planning? Tax planning is the process of projecting out your future income to determine strategies for how to pay the least amount of tax overall, either during your lifetime or a period of years.

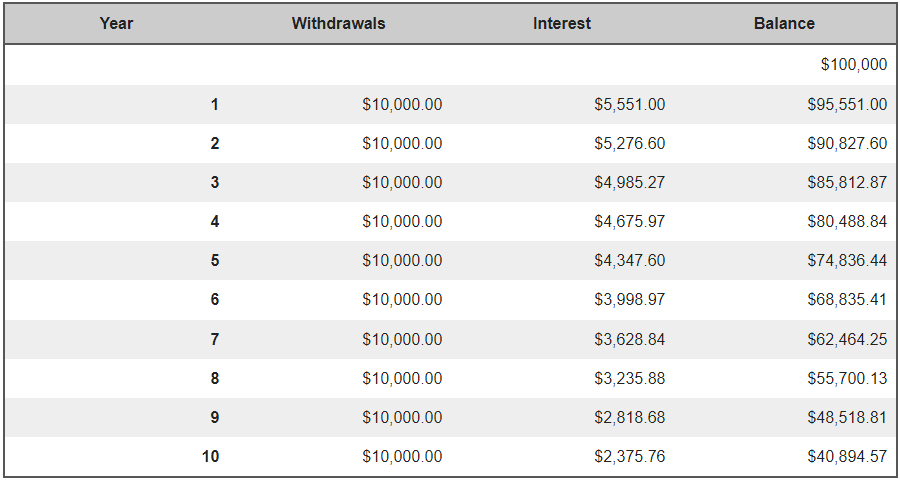

Example: Inherit $100,000 IRA

The table below shows the projections of taking equal distributions of $10,000 for each of the ten years. All remaining funds are then required to be withdrawn in year ten. Assuming a 6% growth rate on the account, this would leave over $40,000 still in the IRA which would all need to be taken out and become taxable in year ten!

Income tax planning may reveal a more ideal withdrawal amount for each year, depending on your other taxable income. For example, another strategy could be to fully deplete the account before turning on other income sources such as a pension or Social Security, so your income tax bracket does not jump once those incomes begin. Clearly, tax planning is needed to make smart financial decisions about how much you should actually withdrawal each year based on your personal circumstances.

![]() Thanks for visiting! Schedule an Introductory Call to discuss what you want to accomplish and to see if we are a good fit.

Thanks for visiting! Schedule an Introductory Call to discuss what you want to accomplish and to see if we are a good fit.