Not all inherited assets are created equal, and there are particular rules regarding required withdrawals when it comes to IRAs.

1) Determine what type of beneficiary group you fall into:

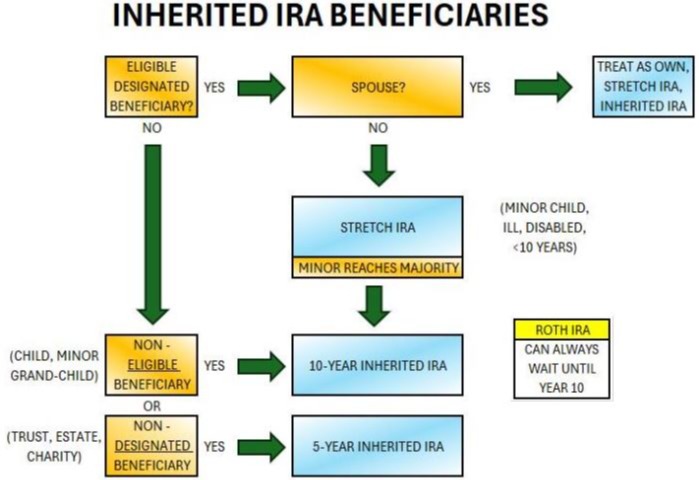

Eligible designated beneficiary – These include surviving spouses, beneficiaries not more than 10 years younger than the decedent (maybe you inherited it from your older brother), certain minors and disabled or chronically ill individuals. For these beneficiaries, the old rules from prior to the 2020 SECURE Act still apply, and they are generally able to stretch distributions over their remaining life expectancy. Only the spouse of the deceased can rollover an inherited IRA into their own IRA. For all others, an inherited IRA must always be kept as a separate account.

Non-eligible designated beneficiary - All of the other human beneficiaries named on an IRA account, most commonly the children, friends or other family members. This type must empty the account within 10 calendar years starting with the year after the death of the original owner.

Non-designated beneficiary – These generally include entities such as estates, charitable organizations, and trusts that are listed as beneficiaries. This type must empty the account within 5 calendar years starting with the year after the death of the original owner.

2) Calculate the correct distribution amount:

In order to calculate required distributions, two pieces of information will be needed: 1) the prior year-end account value and 2) life expectancy. You need to find the life expectancy factor (number) based on your age in the year after the IRA owner’s death. For non-eligible beneficiaries use the IRS Single Life Expectancy "Table I" found in IRS Publication 590‑B. This only needs to be done once and each year that follows you will just subtract one from the prior year’s factor. ("Table II" - The Joint Life and Last Survivor Expectancy is for IRA owners whose spouses are more than 10 years younger and are the sole beneficiaries of their IRAs. "Table III" - The Uniform Lifetime is for use by unmarried owners, married owners whose spouses aren't more than 10 years younger, and married owners whose spouses aren't the sole beneficiaries of their IRAs).

3) Plan for the taxation of distributions:

All withdrawals from your new inherited IRA will most likely be taxable, and these withdrawal amounts would be added to your income for the year of the withdrawal. Consider taking money out of the IRA during low income years to minimize income taxes. Spending money from this account early on may also allow other retirement accounts, pensions and Social Security to continue to grow.

4) Other considerations:

Roth IRA owners don't need to take RMDs during their lifetimes, but beneficiaries who inherit Roth IRAs must distribute the account by the end of the 10th year. Generally, Roth IRA distributions are not taxable no matter who ends up taking the distribution.