The introduction of the 10-year distribution requirement for inherited IRAs of non-spouse beneficiaries has brought forth a fresh set of opportunities and challenges for inherited IRA beneficiaries. However, tax planning help to limit how much goes to the IRS, is here!

In 2019, the SECURE Act removed the ability for most non-spouse beneficiaries to stretch required inherited IRA distributions (RMDs) over a lifetime, and now all of the money needs to be withdrawn by the end of the 10th year after death (for deaths in 2020 or later). If the original owner had started RMDs, beginning in 2025 annual RMDs are required for years 1-9, and the full IRA account balance has to be withdrawn by the end of the 10th year.

So, whether you are inheriting a $100,000 IRA or a $1 million IRA, you have to fit that amount of income from IRA withdrawals into the next 10 years! See the need for some serious tax planning? Tax planning is the process of projecting out your future income to determine strategies for how to pay the least amount of tax overall.

If you inherit an IRA as the child or grandchild of the person that passed, you are considered a ‘Non-Eligible Designated Beneficiary’, meaning you are not eligible to stretch the withdrawals over your lifetime, as was the case before 2020. See What Comes Next After You Inherit An IRA? for more details about beneficiary types.

Here are three scenarios with contrasting 10-year withdrawal strategies, and the difference in the total amount of federal taxes paid is staggering! In all scenarios the assumptions are the beneficiary has inherited $500,000 in pre-tax IRA assets, 6% account growth, and $125,000 in taxable income from working (placing them in the 24% federal income tax bracket as a single filer).

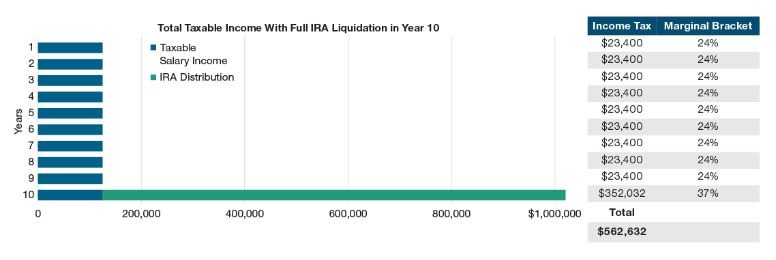

Scenario 1 - The original IRA owner had not yet reached their Required Beginning Date, and, therefore, no RMDs are required for the beneficiary. No withdrawals are taken in years 1-9, then full liquidation in year 10. Total federal taxes over 10 years = $562,632

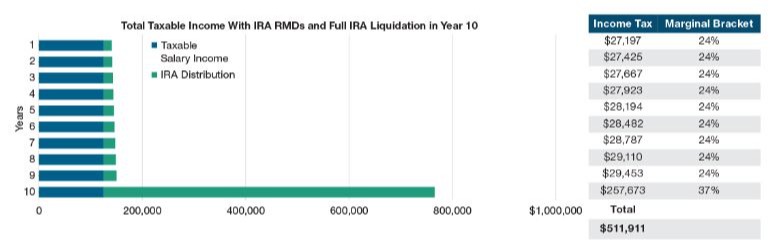

Scenario 2 - The original IRA owner had reached their Required Beginning Date, and, therefore, RMDs are required for the beneficiary starting with the year after death. Only RMDs are taken in years 1-9, then full liquidation in year 10. Total federal taxes over 10 years = $511,911

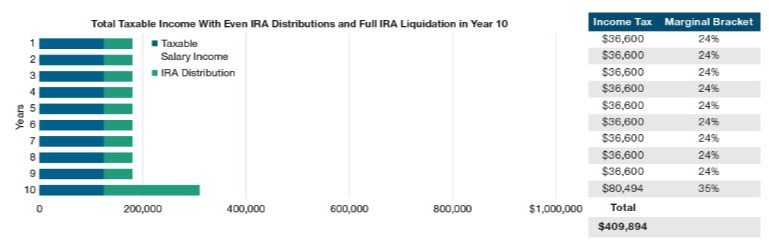

Scenario 3 – Each year $55,000 is taken to spread out taxes, but stay within the beneficiary’s current 24% tax bracket. Then full liquidation of the remaining balance in year 10. Total federal taxes over 10 years = $409,894

In summary, when in doubt, spread it out! Scenario 3 resulted in $152,738 less tax than Scenario 1!

There are pros and cons of taking early, late, or equal IRA withdrawal amounts each year. Income tax planning may reveal a more ideal withdrawal amount for each year, depending on your other taxable income. You should consider other factors such as when you plan to retire, start a pension or Social Security, and other factors that are unique to your personal circumstances. Clearly, tax planning is needed to make smart financial decisions about how much you should actually withdrawal each year, once you know if there are any required annual withdrawals. At Whitford Financial Planning, we develop customized withdrawal strategies based on your overall financial goals and situation.

All investments are subject to market risk, including the possible loss of principal. All charts and tables are shown for illustrative purposes only. T. Rowe Price Investment Services, Inc., distributor.

![]() Thanks for visiting! Schedule an Introductory Call to discuss what you want to accomplish and to see if we are a good fit.

Thanks for visiting! Schedule an Introductory Call to discuss what you want to accomplish and to see if we are a good fit.